With more and more millennials entering the home-buying market, they question whether their student loan debt will hinder the process. Student loan debt affects about 42 million Americans, totaling $1.64 trillion in the U.S alone.

Large debt can make it difficult for young adults to reach such large financial milestones, like owning a home.

Despite this, the dream of homeownership remains a priority for many potential buyers. Though student loan debt is a hurdle many face, homeownership is still achievable.

In this article, we’ll take a look at how student debt can affect getting a mortgage, as well as tips for graduates and current students looking for strategies and options to help them reach homeownership.

The Federal Housing Administration announced updates to its student loan debt calculations, making FHA mortgages much more obtainable for student loan borrowers.

The policy change removes the current requirement that FHA mortgage lenders must include 1 percent of the outstanding student loan debt while calculated the borrower's monthly debt obligations. Borrowers in an approved deferment or forbearance who are only under an income-based repayment plan are included.

The policy change would mean that underwriters will no longer assume that the actual monthly debt of the borrower's student loan is 1 percent of the total balance during the FHA loan underwriting process.

For example, let's say you have an outstanding student loan debt balance of $50,000, but you're approved under a deferment plan to only pay $200 per month. With the old underwriting guidelines, a monthly debt of $500, which is 1 percent of $50,000, would be counted. Now, underwriters must use the actual amount you are permitted to pay. This policy change opens the doors to borrowers with a lower overall credit profile and a higher debt obligation to be a homeowner.

Before looking to purchase a home, it’s important to know the impact student loans have on qualifying for a mortgage and how lenders will determine your affordability when you have these debts.

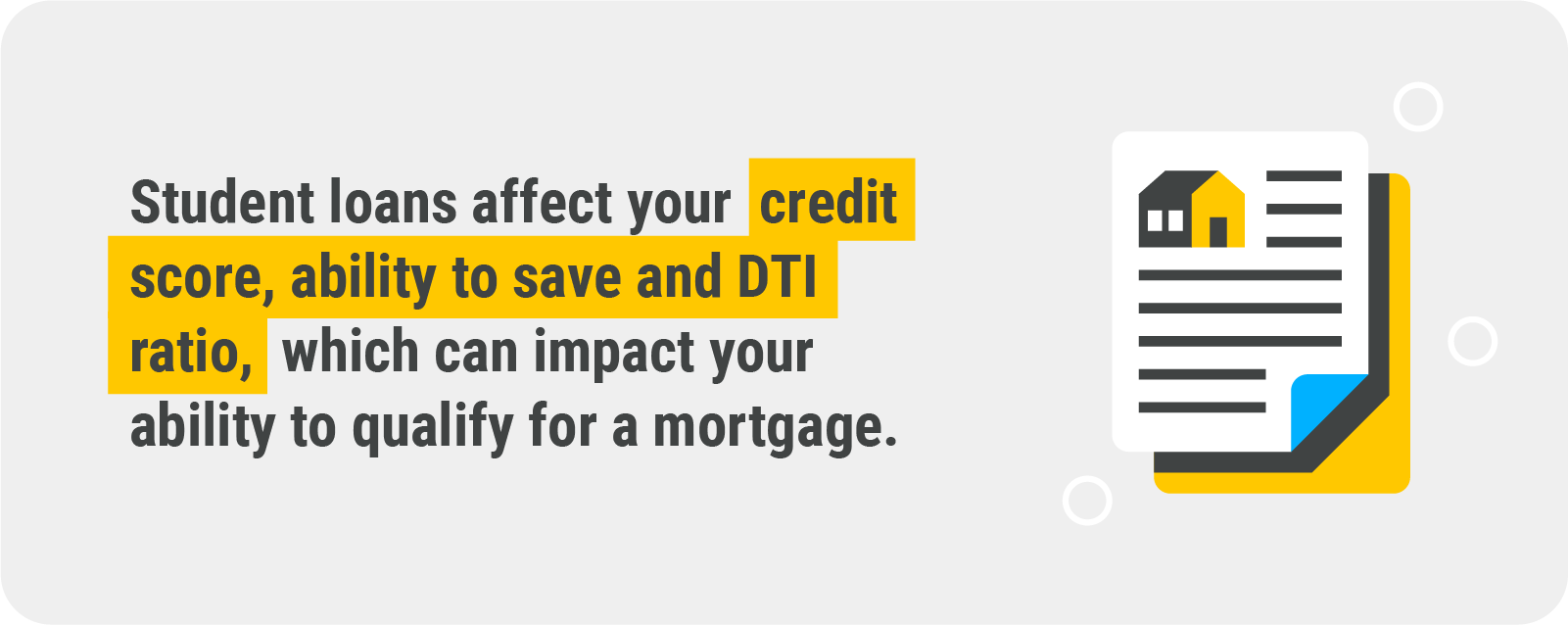

While having student loan debt doesn’t stop your ability to qualify for a mortgage, it does affect your debt-to-income ratio (DTI), credit score and ability to save, which are key components associated with purchasing a home.

Student loan debt is no different from any other debt, and lenders will look at it as such. For example, missing student loan payments can affect your credit history and, in turn, impact your ability to qualify for a mortgage. Or, if your DTI ratio is on the higher end of the scale, it can affect a lender’s decision to move forward with a loan.

The only time your student loans may impact your eligibility to qualify for a mortgage is if you’re in default. Defaulting on a loan means you have failed to make a payment on your loan in 270 days. This will have a drastic impact on your credit score, making it less likely for a lender to approve you for a mortgage loan.

As mentioned, debt is a huge factor mortgage lenders look at to determine your eligibility. Lenders want to know that you will be a trustworthy borrower and can successfully pay back your loan. Lenders will pull your credit report and financial history to help them make an informed decision.

Here are a few things lenders may look at when qualifying you for a mortgage:

If you’re in a position where you’re able to pay down your debts first, that may be the smartest solution. While you can still apply for a mortgage with student loan debt, working towards paying all or some of it off can help you qualify for a better mortgage rate. As mentioned, student loan debt affects your DTI ratio, credit score and ability to save.

Taking on a home loan will add to your already existing debt, which can increase your DTI ratio. If you have a high DTI ratio, the smartest solution would be to get it down to a reasonable percentage before applying for a home loan.

Don’t let having student loan debt discourage you from qualifying for a loan. Depending on your income, you may still be able to pay your student loan payments on time and afford a monthly mortgage payment. It ultimately comes down to your income and how comfortable you are taking on the extra debt.

Though student loan debt can make the home-buying process a bit more challenging, it is doable. Follow the tips below to learn strategies that can help you qualify for a mortgage.

Since FHA loans only require a 3.5 percent down payment and have more relaxed qualifications than other loans, it makes buying a home with student loan debt more affordable. Even though the requirements to qualify for these types of loans seem more attainable, there are FHA student loan guidelines to be aware of when qualifying.

Lenders will ask you or the loan creditor to provide documentation of your loan balance, required monthly payment and loan status. When determining your eligibility for the loan, lenders will either calculate your monthly payment into your DTI ratio, or they’ll take one percent of the total loan balance and use that number to determine your DTI ratio.

If your loan is in default, you likely won’t qualify for an FHA loan.

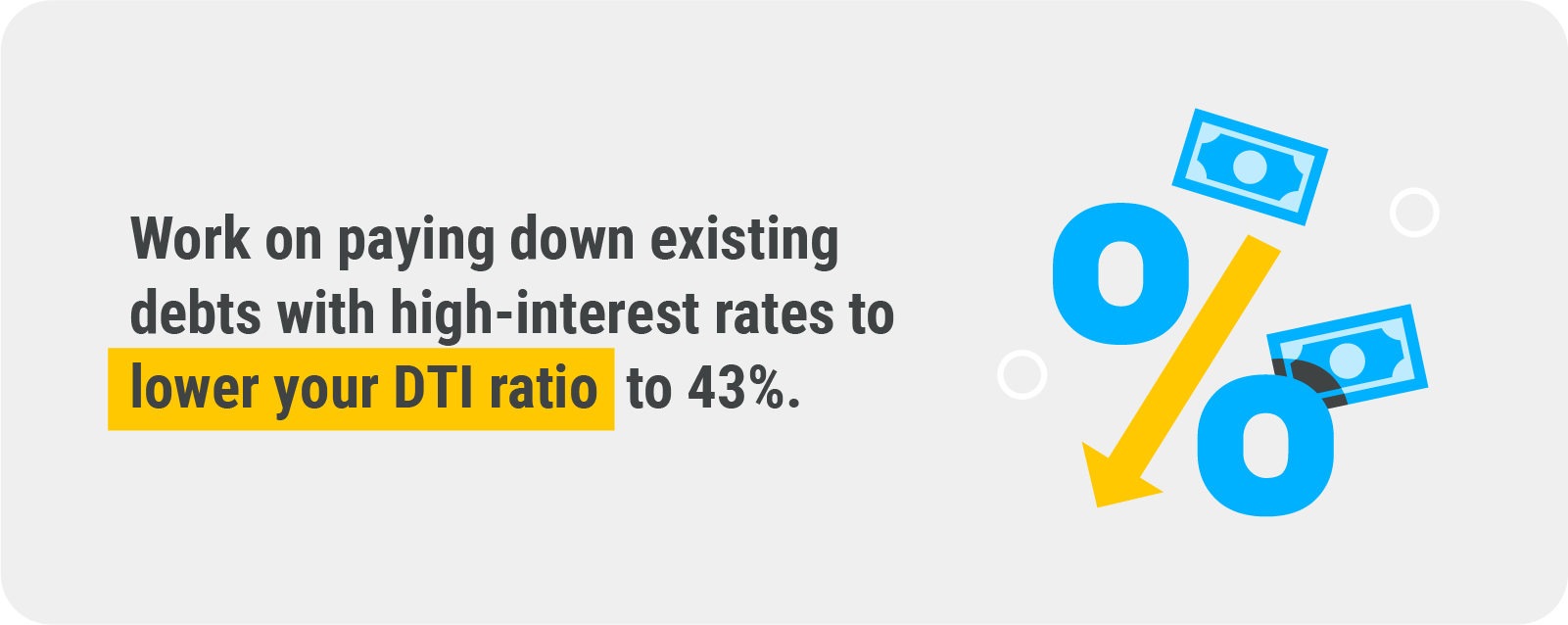

Lenders will look at your income before taxes and compare it to your existing debt, and the more debt you have, the higher your DTI ratio. To qualify for a mortgage as a first-time homebuyer, lenders recommend that your DTI ratio is below 43 percent. Consider paying down some of your existing debts, like a car loan, credit card bill, or other personal loans, to lower your DTI ratio quickly.

Prioritize paying off your debts with high-interest rates first. Doing this will help you lower your overall DTI ratio while saving money you would have paid in interest down the line.

When saving to buy a house, avoid opening any new lines of credit and adding to your existing debts. Focus on lowering the debt you have to put yourself in a healthier financial standing.

Another way to lower your DTI ratio is to increase your income. While you may not be getting a huge raise at your current job anytime soon, picking up extra cash here and there can help. Try picking up a side hustle or taking on overtime hours at work.

When applying for a loan, you will need to prove that this is regular, consistent income for it to apply to your DTI ratio. If you’re committed to buying a house even with student loan debt, it’s important to do what it takes to reach your goal.

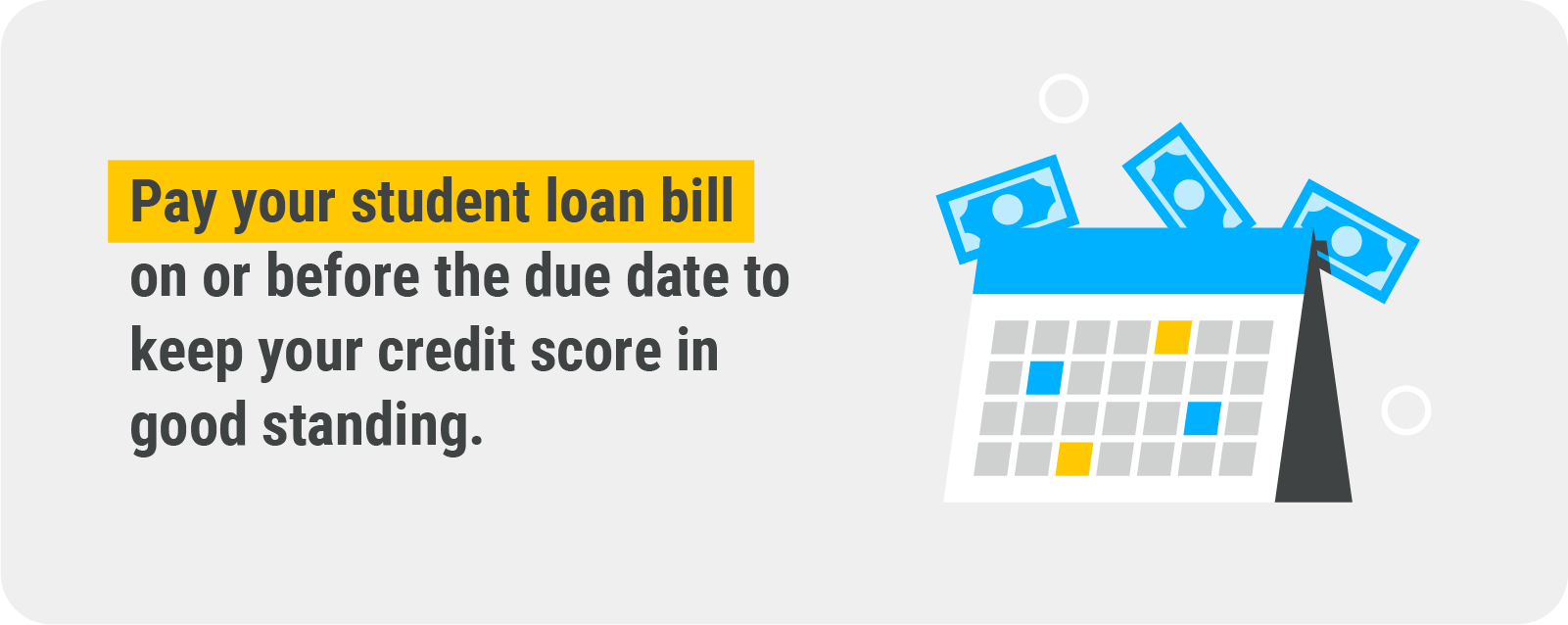

Late or missed student loan payments can affect your credit score, which is a major factor lenders will look to when qualifying you for a loan. The higher your credit score, the better your chances of getting approved for a mortgage at a good rate.

Your ability to make payments on time shows lenders you’d be able to take on a monthly mortgage payment in addition to your existing debts. It also shows lenders you’re a trustworthy borrower given your healthy payment history.

When making student loan payments, pay the full amount on or before your due date to keep your credit score in good standing. To avoid missing deadlines, consider setting up an automatic payment system on your account.

Refinancing works by having a lender pay off your existing loans with a new loan with a lower interest rate. If you have multiple student loans, both private and federal, this can be an excellent option to help you save money by having a lower interest rate and monthly payment.

Similar to purchasing a home, there are certain qualifications to refinance your loans. Some of these requirements include:

It’s important to note that if you’re interested in qualifying for any form of student loan forgiveness, you will not be eligible for refinancing. If you’re able to refinance your loans and save on payments, it can help set you up for success when purchasing a home. Since your rate will be down and your monthly payments may decrease, your DTI ratio will be in better standing.

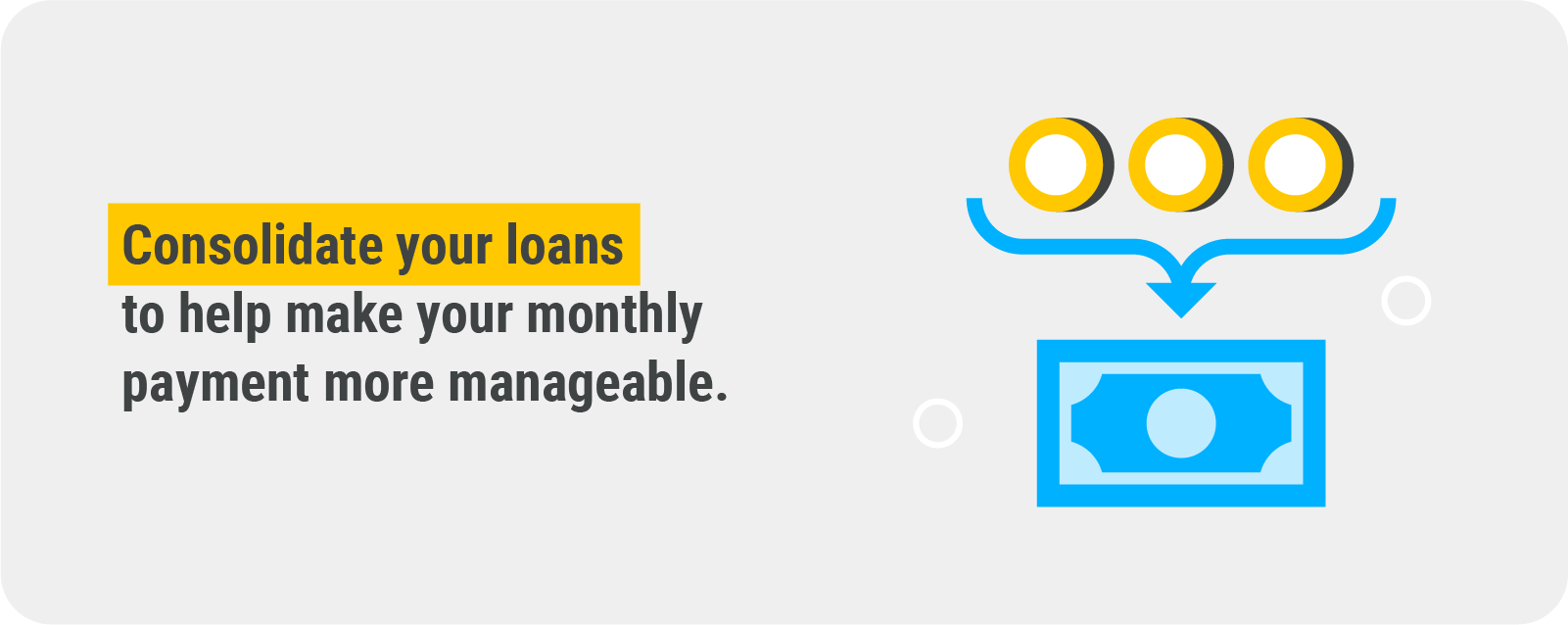

Similar to refinancing, you can also look into consolidating your student loans. Unlike refinancing, you cannot consolidate your private loans, but you can consolidate your federal student loans. Consolidation will combine your monthly payments into one, so you don’t have to worry about making multiple payments throughout the month. There are pros and cons to consolidating your federal loans.

If you’re someone who has multiple loans, consolidating your loans into one payment can help make it easier to manage. By doing this, you could get a lower monthly payment.

When you consolidate your loans, you’ll receive a longer loan term, which means you’ll have more time to pay off your debts. The downside to this is that a longer loan term means you may end up paying more interest over time, which won’t end up saving you money.

Consolidation is best for those looking for a more manageable monthly payment to help them afford to save for a home or make a monthly mortgage payment.

Income-driven repayment plans base your monthly student loan payment on your monthly income and family size. This is a good plan for parent homebuyers who still have student loan debt and want to purchase a family home.

You can apply for many different income-driven plans, each of which takes out a different percentage of your discretionary income. Discretionary income is what is left after you account for taxes and necessities.

The income-driven repayment plans available to borrowers include:

Though these payment plans can give you a lower monthly payment, you will receive a longer loan term. Similar to consolidation, this means you may pay more interest over time, which is an important factor to consider.

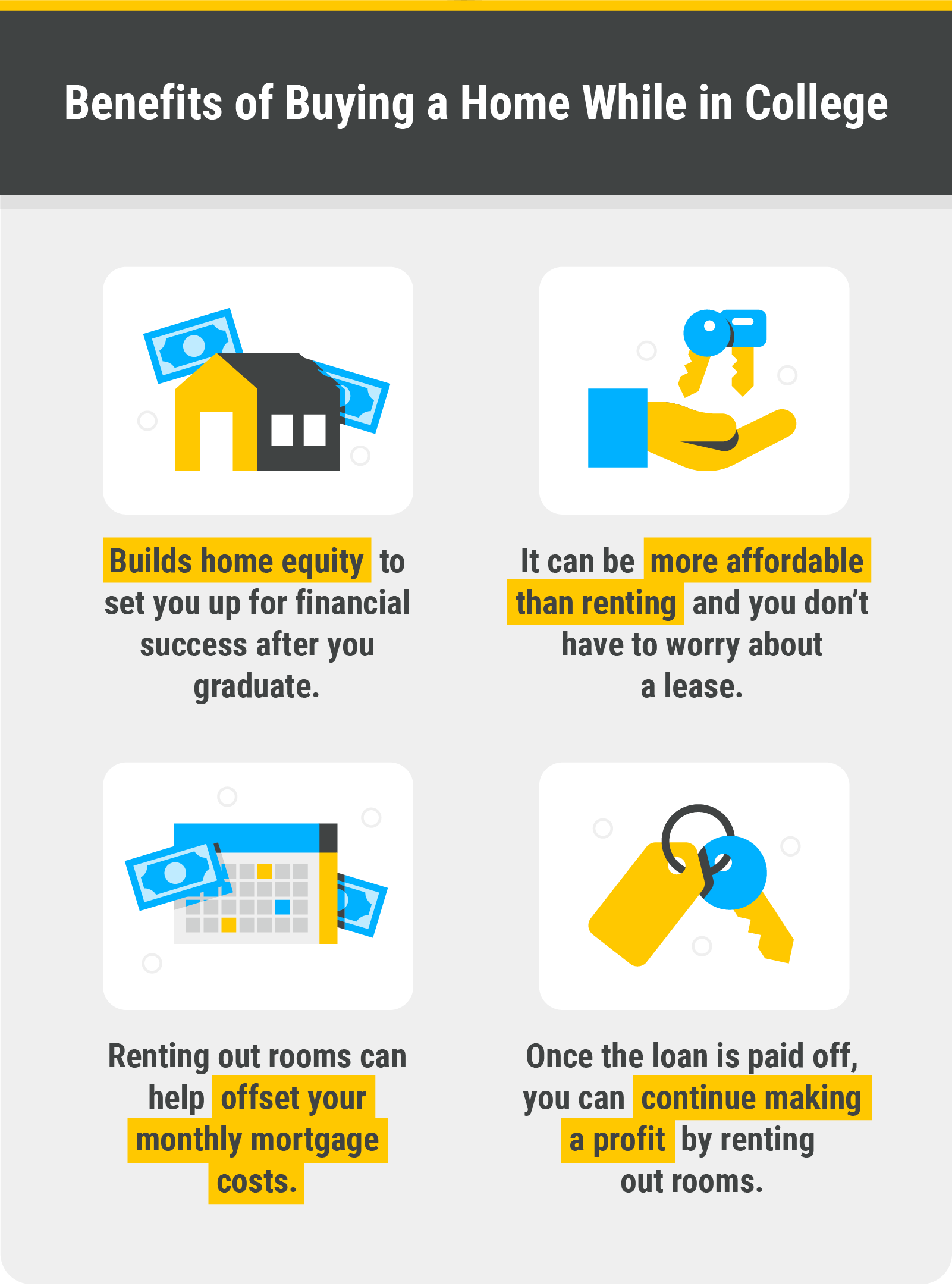

If you’re still in college and have yet to start your student loan payments, you can still qualify for a home loan to better prepare yourself for your future. Buying a home in college has many benefits and can build your home equity. Here are three actionable steps you can take today to qualify for a mortgage as a college student:

Good credit is one of the most important aspects of qualifying for a home loan. Establishing good credit early on can help prepare you for big financial goals, like buying a home.

College credit cards are available to students with limited credit history who are looking for ways to build their credit while still in school. Generally, these types of cards are easier to obtain than other credit cards, and they have more flexible requirements.

Another great way for students to build their credit is to become an authorized user on a parent or family member’s credit card. As an authorized user, you can make purchases and use a credit card as if it were your own, but the primary cardholder remains legally responsible for paying the charges. To keep your credit health in good standing, make sure all debts are managed responsibly by making payments on time and in full.

As a student, you may only be able to work a part-time job, which means your income may not be as significant as if you worked full time. Getting a co-signer can help your chances of qualifying for a mortgage despite your monthly income. A parent or family member who has good credit and a sufficient income can co-sign on the loan and help you secure a better mortgage rate.

Once you’ve secured a mortgage, you can rent out the extra rooms in your home to help make your monthly mortgage payment more affordable. This will also help you contribute to lowering the overall loan balance you’ll have once you graduate.

Renting apartments or rooms in a home is typically pricier in college areas, so this can be a great alternative to give you a place to live while having the extra rooms rented out. You also won’t have to worry about paying rent and signing a lease every year.

Since homes usually increase in value over time, you can make a profit if you continue to rent it out or if you decide to sell it later down the line.

Determining whether you should buy a home with student loan debt comes down to how comfortable you are with the added financial responsibility. Though buying a home sometimes means cutting costs in other areas, you shouldn’t take on more debt if you cannot live comfortably within your means.

If you’re afraid taking on more debt may be too much, consider waiting to buy a home until you’re in a better financial position. If you’re able to increase your income and comfortably take on the responsibility of becoming a homeowner, look into programs that can help you get there.

To reach your goal of homeownership, applying for an FHA loan can help make it more affordable — check your eligibility today to see if you qualify.

Buying a home can be a tricky process, especially when you have student loan debt. We’ve compiled a list of resources to help you understand other strategies to help increase your chances of affording a home while still paying down your student loan debt: