Buying a home is a huge milestone, and deciding whether or not you’re ready to take that leap can sometimes be difficult, especially in today’s climate. There are many things to consider when making such a huge decision, including your personal finances and the state of the market. Though we’re living in such unpredictable times, many Americans are still on the hunt for a new home. The U.S homeownership rate reached 65.4 percent in 2021, according to the U.S Census Bureau. Of those homeowners, 33 percent were first-time homebuyers based on reports from the National Association of Realtors.

Before deciding if you’re ready, you need to educate yourself on what becoming a homeowner entails. Some buyers jump into the process without fully knowing how big of an investment home buying is. In fact, the NAR found that in 2021, three percent of homebuyers wished they would have waited to buy a home. The more you know, the more prepared you’ll be.

Timing matters when purchasing a home, especially your first one. Here are six questions to ask yourself to determine whether you should buy a house now or wait.

The housing market is always changing, so it’s essential to do your research on where the housing market stands in your area. When determining if interest rates are working in your favor, you will want to look at the current mortgage rates. When mortgage interest rates are low, you will end up paying less in the long run, making it a better time to buy.

In 2021, mortgage rates were as low as 2.25 percent. This puts buyers in a good financial position because it could make their monthly payments more affordable.

You also want to pay attention to whether the area is currently in a buyer or seller’s market. If you’re in a seller’s market, this means that there are more buyers than there are sellers. Since the demand exceeds the supply, home prices typically increase. Because of this demand, it makes it hard for buyers to be able to negotiate prices with sellers.

On the other hand, a buyer’s market means that the number of houses for sale exceeds the number of buyers in the market, so the supply exceeds the demand. Typically, homebuyers want to buy in a buyer’s market because sellers are more willing to negotiate on prices, and there are more options available.

Your financial preparedness is important when it comes to buying a home. You want to make sure your finances are in good standing and you’re able to follow through on such a big financial commitment. Lenders look at your current income and employment history when deciding whether to approve you for a loan. They do this because they want to make sure you’re going to be able to cover the cost of your mortgage now and in the future.

Lenders typically look to see if you’ve been at the same job for at least two years. This proves stable employment, making it easier for them to trust that you’ll be able to afford your payments.

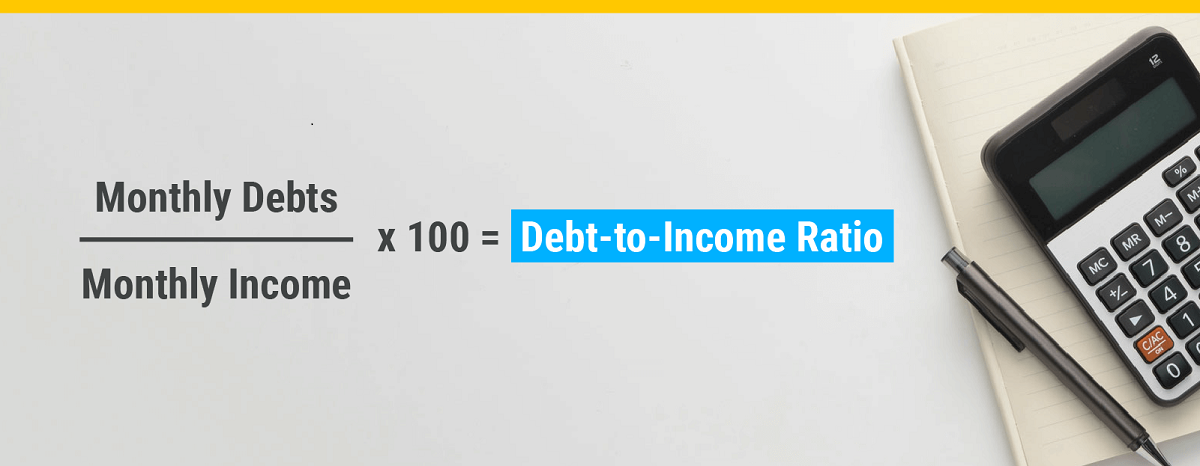

Another important factor that lenders take a look at is your debt-to-income ratio (DTI). This is important because it allows lenders to determine whether you will be able to afford another loan.

A general rule of thumb is to have a DTI ratio at or below 43 percent. If your DTI ratio is above that, you may want to consider lowering it before trying to qualify for a home loan.

To calculate your debt-to-income ratio, add up all of your monthly debts and divide that number by your total monthly income. Once you have that total, times it by 100, and you will get your DTI percentage. Though the recommended DTI ratio is 43 percent, it depends on the lender. When going with an FHA loan, some lenders may be more lenient when it comes to your DTI ratio.

Aside from your income and debt, you’ll want to make sure you have enough savings to go through the entire home buying process, as there are many costs and fees associated with purchasing your first home.

First, you’ll want to make sure you have enough money to cover the down payment. Most people who are new to home buying automatically assume they need a 20 percent down payment, but that isn’t true. An FHA loan allows you to purchase a home with as little as 3.5 percent down.

From there, you’ll want to factor in closing costs. There are some instances where the seller will cover these costs for the buyer, but you should always make sure you’re overly prepared.

Additionally, some lenders may ask for mortgage reserves. Reserves are not always required, but may be requested by lenders to help you get your application approved. Mortgage reserves are similar to an emergency fund. They are savings you can show a lender to prove you have enough cash on hand to cover your home’s costs should any unexpected incidents occur, such as losing your job or dealing with an unexpected medical bill.

Prospective homebuyers should also take their credit score into account. A credit score of 580 or higher is usually the minimum credit score needed to qualify for an FHA loan, but those with a score as low as 500 can still qualify.

It’s important to determine if you’re ready to settle down in one place. After buying a home, it’s recommended that you stay for at least five years.

When owning a home, you don’t have the luxury of hopping from one place to another like you do when renting. You should be committed to staying in one place to keep up with household maintenance and other responsibilities associated with being a homeowner. If you plan to move within the next few years for any reason, waiting would probably be your best option.

You may have enough savings, have stable employment, a great credit score and think you’re ready to buy a house. If you’ve gotten to this point, it’s important to consider all of the costs that come into play once you become a homeowner. Aside from your monthly mortgage payment, there are plenty of other costs that you need to factor in, like:

Every homeowner must pay property taxes, and some lenders will typically include them in your monthly mortgage payment. If they don’t, you can request it so you don’t have to worry about paying your property taxes in full come tax season.

Similar to property taxes, you can request that your monthly mortgage payments include your homeowners insurance. Even if it isn’t included, you’re still responsible for it.

Whether or not you will pay HOA fees depends on where you decide to live. Typically, you’ll expect to pay HOA fees if you purchase a home in a larger community or development, such as townhomes or condos. These fees will usually cover the costs of maintaining shared areas, like gyms, pools and landscaping.

Garbage, electricity, gas and water are all your responsibility to pay once you become a homeowner. Though not included in your mortgage payment, these costs are important to factor into your monthly budget to determine what you can afford.

If you’re a first-time homeowner, you may be used to renting, where property maintenance was taken care of by your landlord. Now that you will own your own property, it is now your responsibility to keep up with regular maintenance and fixes around your home. Though this may not cost much, these costs can add up, especially if you purchase a home that needs some work.

If you answered yes to the questions above, congratulations, you’re probably ready to buy a home! If not, don’t worry. Sometimes waiting a little longer will put you in the best position to buy a home in the future. If you decide to wait, here are a few things to consider to ensure you’re on the right path to homeownership.

Research and education are key when preparing to buy a home and making such a huge investment. Do your research and brush up on important home buying terms so you know exactly what you’re getting yourself into. Home buying is not an easy process, and it takes a lot of time and preparation. The more prepared you are, the smoother the process will be for you.

The most important part of diving into the home buying process is making sure you have your finances squared away.

As mentioned, you should have stable income and employment, a fair credit score, enough money saved for a down payment and closing costs, and your debt-to-income ratio should be below 43 percent.

If you find yourself unable to reach these financial requirements, spend some time working on getting these numbers to where they should be.

Ensuring you’re in a comfortable financial position will help take the stress and worry out of the home buying process and make it more enjoyable.

One mistake new homebuyers often make is failing to get prequalified before looking for homes to buy. Getting prequalified will allow you to see what you’re able to afford, making it easier to look for homes that are realistic to your budget. You would hate to be in a situation where you absolutely loved a house, only to find out you couldn’t afford it. To minimize the chances of that happening, always get prequalified before shopping for homes.

There is so much to learn when it comes to purchasing a home and sometimes it can be hard to determine whether or not you’re ready. We’ve gathered insight from industry professionals and homebuyers to find out the biggest lessons they learned and tips that they wish they would have known.

Sometimes new homebuyers get so excited about this new journey that they often rush through it and overlook important steps.

“Looking back at my first-time home buying experience, I wished that I hadn't been in such a rush and had the time to slowly evaluate each property properly,” said Albert Lee, founder of Home Living Lab. “Ultimately, a home purchase is a huge investment and there are so many areas to consider. For an inexperienced homebuyer like myself, I should have done my due diligence better even though it would take more time.”

Many homebuyers agreed that taking your emotions out of the process is always a good idea. It’s important to remain realistic, stay within your budget and be patient with the process.

Jen Breitegan, founder of Organize Envy said, “My advice for first-time buyers is to try to remove emotion from the process and make sure you’re buying a home that you can truly afford, doesn’t need more work or repairs than you can take on, and is in an area you will want to live in long-term.”

Besides the market, considering all costs will save you the headache of wondering how much you can truly afford.

With so many additional costs you need to factor in, coming up with a budget and sticking to it is key. Ren Lenhof from House Fur said, “We stuck with our budget the entire time and made sure that we would still be able to ‘have a life’ and pay our mortgage. We never let the financial burden of owning a home give us any stress.”

Every homebuyer’s journey is different, and determining the right time to buy is a personal decision that only the buyer can make. With the fluctuating market, do your research and make sure you have your finances in a comfortable position.

Remember to remove your emotions from the process and be realistic with yourself. Following the tips in this article can help you decide whether or not you’re ready to dive into the new journey of homeownership. To see if you qualify for a low money down mortgage, check your eligibility for an FHA loan today.