Starting your college journey is a time full of significant life changes and weighty choices. A big decision when going off to college is deciding where you are going to live. It’ll likely be your first time living on your own, and searching for a new place to live can be very exciting.

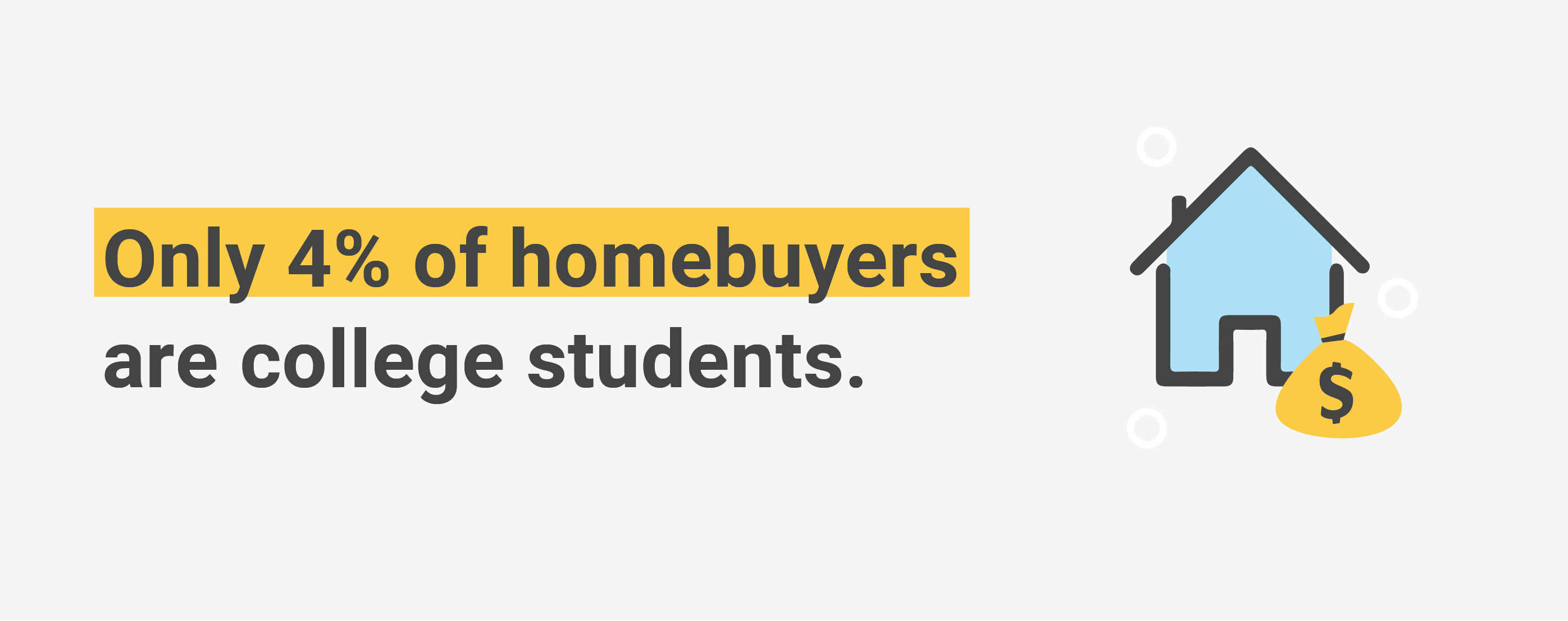

Renting or living in a dorm may seem like the obvious choice for many, but deciding to purchase your own home can have a slew of positive financial benefits. As of 2019, college students made up 4 percent of homebuyers in the U.S. While this percentage may seem low, it proves there may be a missed opportunity for students looking for housing.

Deciding to purchase a home over renting an apartment can be a difficult decision. To buy a house, you'll need a good credit score, steady income, and the finances for a down payment.

Homeownership in college isn't the right choice for every student, and it's essential to understand its risks.

Yes, it is possible to purchase a home while in college, bearing the individual has the appropriate financial background and meets the lender’s requirements. It takes time and money to keep up with such an investment, but this may be an excellent choice for you if you meet the criteria.

Generally, to be a good candidate for homeownership, you should have:

Using part-time income to obtain a mortgage is possible. However, lenders typically approach part-time income more cautiously than a full-time income. Expect your lender to take a detailed look at your part-time income and the consistency over the past two years.

Many college students may not have an established credit score yet. Some lenders might be willing to look at alternate tradelines to determine whether or not you are a likely candidate for repaying your debts on time.

Lenders open to alternate tradelines will look at your payment history on items such as utility bills, rent payments, renter’s insurance, car payments, or more to determine your eligibility.

Note: guidelines can vary depending on the lender, loan type and other factors. Some lenders may not allow alternative tradelines or part-time income.

Having a co-signer on your loan is a smart financial move for college homebuyers. A co-signer can be a parent, guardian, or significant other with a stable income and a good credit score. If you lack substantial income and can't get a mortgage on your own, you may still qualify for a mortgage with a co-signer.

The co-signer is there for backup if you run out of funds and the bank needs someone to pay the money. Keep in mind that you are still responsible for the payments and need to keep up to date with them.

Renting a home comes with certain limitations, but you are free to make decisions for yourself without risking your security deposit if you are the homeowner.

Buying a house in college can be an excellent idea for many reasons. If you purchase a home close to campus or where college students typically live, you may be able to keep this home for many years and lease the rooms. College students will always need housing, and you can provide that for them.

One of the most liberating parts of owning your own home in college is the ability to make permanent or drastic design changes. Do you want to paint your bedroom? Go for it. Do you think the carpeted living room would look better with hardwood floors? The choice is all yours.

Being able to choose your roommates is a great perk to buying your own home. You might have a few friends who want to live with you throughout college, or you may want to start fresh and find roommates online. Either way, you can pick and choose roommates who best suit you and your lifestyle.

It is a huge relief to know you won't have to pack up your belongings, move, and redecorate each college year. You will be able to have your own space and privacy that many students want.

It's possible to pay off your mortgage by renting out the rooms to other students, and in the long run, this can be cheaper than renting an apartment or home.

Take a look at what the mortgage payment would be, and then set the rooms' rent to account for more than the mortgage payment. Buying a home may seem like an unrealistic purchase for a college student, but it could provide an excellent investment for years to come.

An FHA loan is a mortgage insured by The Federal Housing Administration. This mortgage type is traditionally for first-time homebuyers or borrowers without a sufficient credit score or the savings for a conventional loan. With this in mind, an FHA loan is typically an excellent mortgage option for a college student.

The FHA requires homebuyers to have a credit score of at least 500 and 10% down or 580 and 3.5% down. However, the FHA doesn't make the loans; lenders and banks do. In most cases, lenders will expect you to have a 640 credit score or higher. Additionally, the house must meet the FHA's minimum property requirements.

A conventional loan is not secured by a government entity but through private lenders such as banks, mortgage companies, and credit unions.

This type of loan is a good option if you have great credit and the savings to make a significant down payment. Down payments for conventional loans typically range from 5-20 percent.

A VA loan is a mortgage guaranteed by the United States Department of Veteran Affairs, and you must meet specific service requirements to be eligible. VA loans have many benefits, such as no down payment, lower closing costs, and historically lower interest rates.

Being a landlord can be a full-time job. The constant maintenance, potentially problematic tenants, and financial responsibility can make this experience daunting.

If you can make repairs or know someone who can do it for a reasonable price, this can be an excellent investment for you. Before deciding to purchase a home, make sure you can work on the repairs, are easy to work with, and have the time and money to keep up with the property.

Other expenses such as insurance payments and taxes are other payments you need to take into consideration.

Investing at a young age seems like a great idea, but don't go in with the mindset that you'll figure it out as you go. Here are a few questions to ask yourself:

If you answered no to any of these questions, you may want to rethink if you are ready to purchase your first home. You need to think hard about your financial decisions. Everyone's situation is different, but asking yourself these questions can be a good starting point to help you decide if purchasing a home as a college student is right for you.

Roughly 70 percent of college students take out student loans. If you fall into that percentage, don’t fret, you may still be able to qualify for a home loan. Tips to increase your likelihood of landing a mortgage with student loans include:

Not everyone is a good candidate for purchasing a home while still in college. Deciding to own a home rather than rent an apartment or live in student housing is a big decision. There are serious financial implications to weigh, so be sure to take all things into consideration before making any decisions.