Occupancy Requirements for FHA Loans

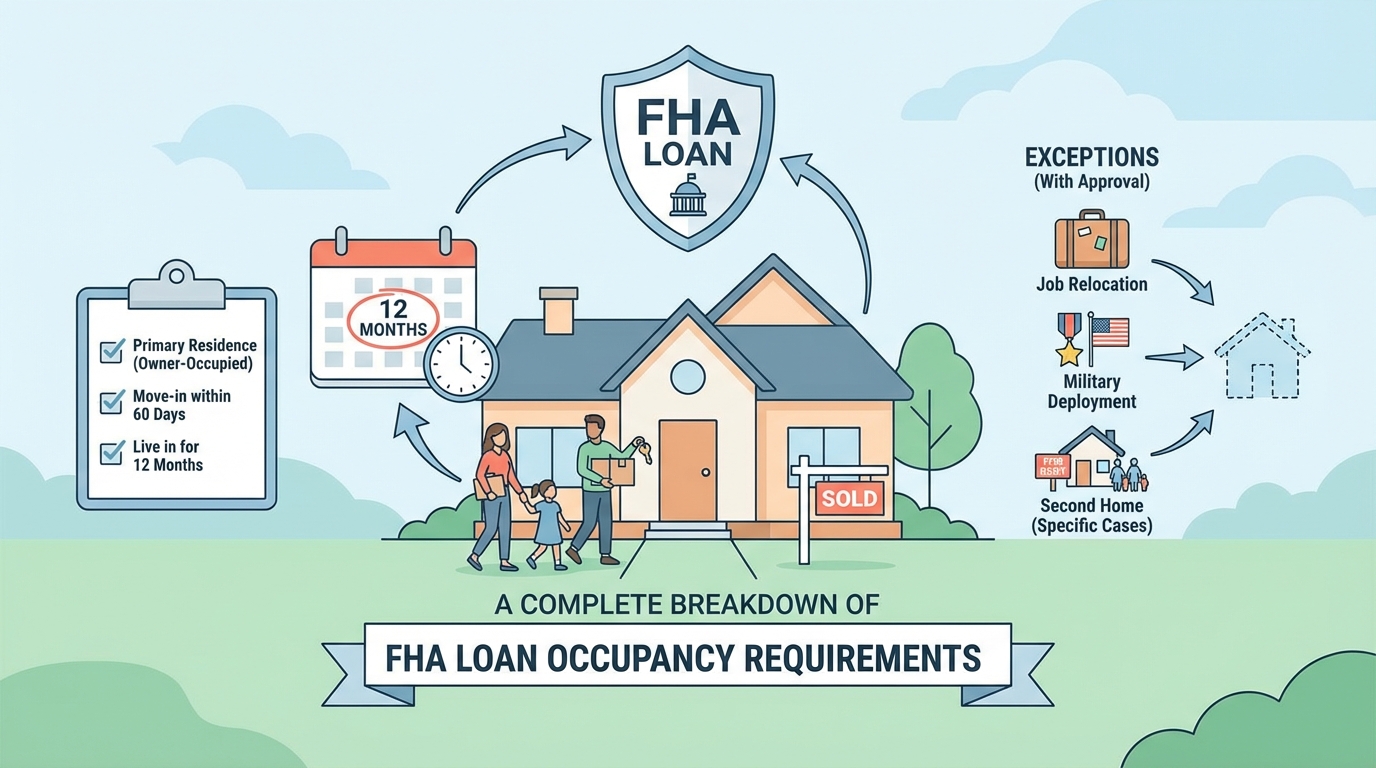

FHA loans are designed to make homeownership more attainable for low- and moderate-income earners. Because of this, they are typically not used for investment properties, vacation homes, or second-home purchases. In most cases, the FHA requires borrowers to use the property they purchase as their primary residence.

The FHA typically requires borrowers to occupy the property they buy as their primary residence for at least one year. By FHA standards, a primary residence is one in which the owner occupies the property for the majority of the year. The FHA also requires that the buyer move into the property within 60 days of closing on their home.

These requirements prevent investors from profiting from the government loan program’s affordable rates and less stringent lending guidelines. Buyers must prove their intent to live on the property (and not use it as a second home or investment) by checking the “Primary Residence” box in the Uniform Residential Loan Application they file with their chosen mortgage lender.

Borrowers are also not allowed to have more than one FHA loan at any given time. If you plan to move out early and purchase another home with an FHA mortgage, talk to a lender about your options.

The FHA requirements state that at least one borrower must reside in the home for at least 12 months. If you’ve purchased a home with a co-borrower, either person could be eligible to move out as long as one person continues to live in the home.

If one co-borrower moves out and wants to purchase another home with an FHA loan, that borrower will need to work with a lender to ensure they meet certain eligibility requirements.

FHA occupancy rules are a little different for condominiums than for single-family homes. To gain FHA approval, condo buildings must have at least 50% occupancy from owners. In some cases, this can be as low as 35%, but the condo association will need to provide documentation for the following:

A few exceptions to the FHA’s occupancy rules exist for military deployment or a job relocation that puts the owner outside a 50-mile radius of the home. Divorce or increased family size (which may require a larger property) could also qualify as exceptions.

If you’re active military and deployed overseas, you’ll still be an owner-occupant if a family member occupies the home or you plan to return to it after your deployment ends.

Another exception is if you are relocated out of state for a job. If this occurs before you meet the one-year requirement, you can still purchase a new home with an FHA loan.

If your family expands due to adoption or the birth of a baby and you have outgrown your current home before meeting the one-year occupancy requirement, you may be allowed to purchase a new home with an FHA loan.

If you and your spouse go through a divorce before meeting the one-year requirement, you have a couple of options. If you and your spouse are co-borrowers, one of you can remain in the home while the other will receive an exemption to purchase another home with an FHA loan. Additionally, an exemption can be provided for both you and your spouse to buy new homes if you need to downsize to make the home more affordable.

In some cases, an FHA loan can be used on a secondary residence — a property the borrower occupies in addition to their primary one. FHA mortgages on secondary homes are only permitted when affordable rental housing is unavailable in the area (or within reasonable commuting distance of the borrower’s work). The maximum loan amount is 85% of the lesser of the appraised value or sales price.

To use an FHA loan on a secondary residence, borrowers must request a hardship exception from the local Housing Opportunities Commission through their lender. The secondary home cannot be a property intended for vacation or recreational purposes.

After occupying an FHA-backed property for at least the first year, owners can use the property as they wish, including renting it out or using it as a secondary or vacation home. Generally, the owners are still limited to one FHA mortgage at a time, even after meeting the one-year occupancy requirement.

To better understand the FHA’s owner-occupancy standards, here are a few common scenarios to consider:

You might wonder how the FHA could ever discover that you violated the occupancy requirements on your FHA loan. After all, it would be impossible for lenders to verify all their loans constantly. While this might be true, there is one crucial aspect to understand.

When you take out an FHA loan, you’re required to agree in writing to the terms of your loan. FHA loan rules specify that occupancy inspections are possible, and if you’re in violation, you may face consequences. Some repercussions include:

Because occupancy inspections could happen at any time, it’s important that you can prove to your lender that you’re living in the home by having any of the following documents available. Each of these will have your name and address and prove that you’ve been living in the home.

FHA borrowers who cannot fulfill their occupancy requirements should discuss their options with their lender. Failing to meet these standards could have legal and financial repercussions without taking the proper steps.