FHA Minimum Property Standards: A Checklist

With an FHA loan, the property must qualify just as much as the buyer.

The Federal Housing Administration backs FHA loans, which help buyers with lower credit scores or limited down payments. However, to use one, the home must meet specific FHA minimum property standards by undergoing a special FHA appraisal.

This appraisal serves two purposes: it estimates the home's market value and verifies that the property meets HUD’s minimum property standards for safety, soundness, and security.

Only if the home passes these checks will the loan be approved.

Every FHA purchase or refinance loan requires this appraisal, which applies to single-family homes, multifamily properties, manufactured housing, and condominiums.

The Department of Housing and Urban Development (HUD) sets FHA minimum property requirements to protect both the borrower and the lender.

For borrowers, these standards ensure the home is safe and livable from day one, without major health or safety hazards like faulty wiring or lead paint.

For lenders, the standards help ensure the property retains value over time. If the borrower defaults, a compliant home is easier to resell and recover the loan balance.

The home must meet the three S’s: safe, sound, and secure. A property with structural issues or environmental hazards may not qualify for FHA financing. To enforce these standards, lenders order an FHA-approved appraisal after a buyer applies for a mortgage. The appraisal confirms both the home's market value and whether it meets HUD’s minimum standards.

HUD periodically updates its standards to address emerging risks. For example, in 2024, new homes in flood-prone zones must have their lowest floor at least two feet above the base flood elevation.

While some buyers may find the standards restrictive, they intend to prevent costly surprises and ensure the home is a sound investment, both financially and structurally.

FHA’s minimum property standards are often summarized as the “Three S’s”: Safety, Soundness, and Security. The property must not endanger the occupant’s health (Safe), must be structurally sound for the long term (Sound), and must have basic security and livability features (Secure).

The home must provide a safe and healthy living environment for its occupants. This means it should be free of health hazards and dangers.

For example, the property should not have pest infestations, toxic materials (such as friable asbestos), or exposed lead-based paint hazards.

Plumbing, heating, and electrical systems must be in good working order to avoid risks (no sparking wires, gas leaks, etc.).

Additionally, the property needs features like sturdy stair rails (so that, say, a steep staircase isn’t a fall hazard) and proper ventilation (attics and crawlspaces shouldn’t harbor mold or trap dangerous fumes).

The home's structure should be structurally sound and free from serious physical deficiencies.

The foundation, walls, and roof should be solid and not in danger of collapse or failure. There should be no ongoing structural issues, such as major foundation cracks, visibly sagging beams, or a roof that’s caving in.

Secure refers to both the security of the property as collateral and the home's physical security.

The property should be secured against the elements and unauthorized entry. In practical terms, windows and exterior doors must be intact and lockable, and any other openings should be covered appropriately. If the home has fencing or railings, they should be in good repair.

The idea is that the home can be safely occupied and protected: for example, a broken exterior door or missing window not only diminishes security but also could let in weather or pests.

HUD sometimes describes security as protecting the property’s value, which overlaps with ensuring the house doesn’t have conditions that would rapidly deteriorate.

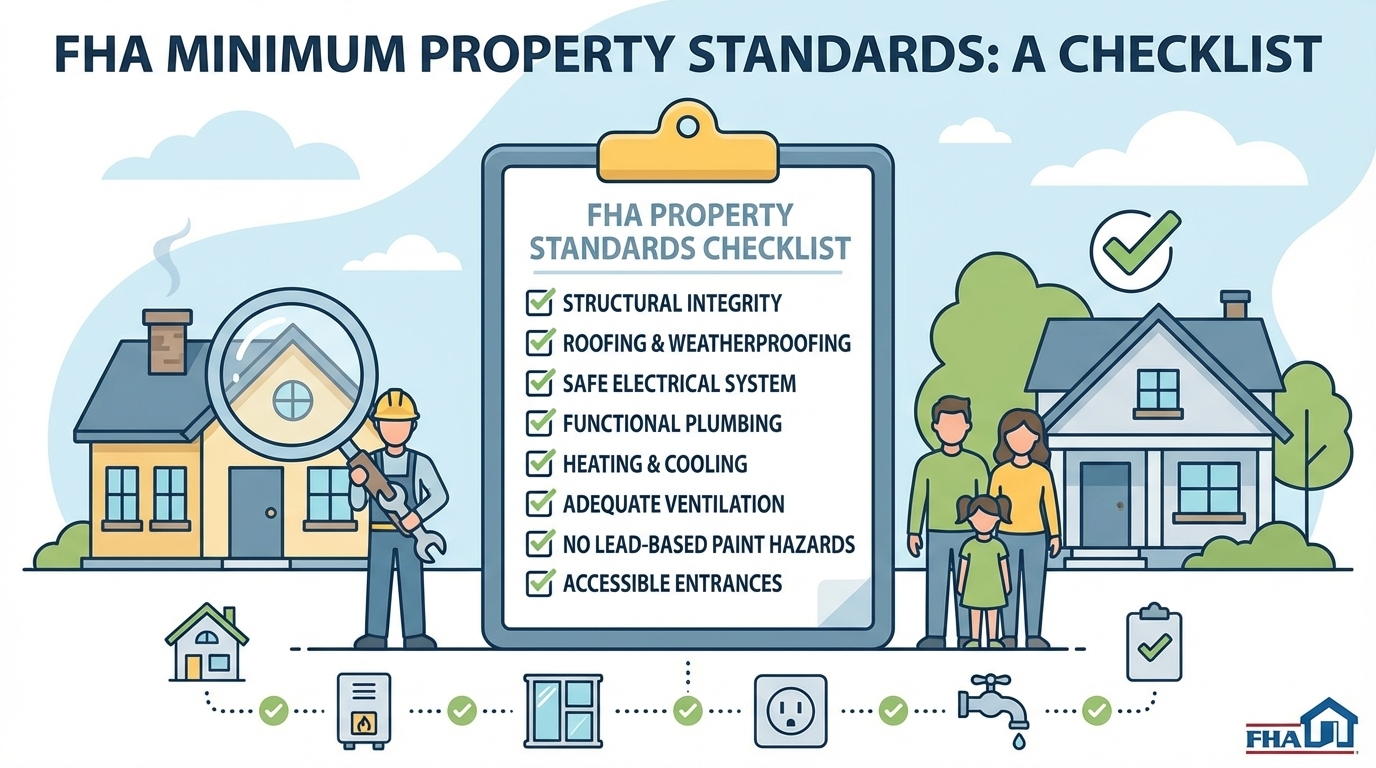

Below is the FHA minimum property standards checklist that outlines what must be functional and up to code for the home to qualify for FHA financing.

If any of these items, from FHA windows and doors guidelines to FHA smoke detector requirements, fail to meet standards, the buyer or seller must make repairs before the loan can be approved.

While FHA’s standards are strict, not every little issue will sink an appraisal.

The FHA does not require sellers or buyers to fix cosmetic or minor defects if they do not affect the home's safety, security, or soundness. In other words, the appraisal report can overlook normal wear-and-tear that is not a structural or health concern.

Here are some examples of minor deficiencies that are generally forgiven or do not require repairs under FHA rules:

Normal “deferred maintenance” (things aging normally) and “normal wear and tear” are not grounds to fail an FHA appraisal. The appraiser may still mention them in the report, but tag them as minor.

What happens if the home you want fails to meet one or more of the FHA’s property standards? Depending on the situation, you can take a few options.

The most common solution is to have the seller fix any FHA-required issues before closing. Repairs like peeling paint or missing handrails are typically handled as part of the sale. If the seller agrees, the appraiser may return to confirm the work is complete.

If the seller can’t afford the repairs, you may offer to raise the purchase price. The seller will then pay for the fixes upfront and get reimbursed at closing from the increased sale price. This allows the home to meet FHA standards without delaying the sale.

Conventional loans may be more flexible on property conditions. If the issues are relatively minor (or if the buyer is ineligible for FHA for other reasons), one option is to apply for a conventional mortgage instead, which doesn’t have the same exhaustive checklist.

In some cases, if the property is really in bad shape (like an unlivable fixer-upper), the only way to buy it might be with cash or a rehab loan because even conventional lenders have some standards (for example, most lenders won’t finance a home with a roof that’s caving in).

The FHA 203(k) program (aka the Rehabilitation Mortgage Insurance Program) is designed specifically for a home requiring a lot of work. With a 203(k) loan, you can finance the purchase of the home and the cost of the required repairs/renovations together in one FHA mortgage.

This program allows for completing minor and major work after closing with the funds from an escrow account in the loan. If the home you love doesn’t meet standards but has potential (and you’re willing to do renovations), a 203(k) loan is a great solution.

One downside is that 203(k) loans involve more paperwork, require licensed contractors for the repairs, and can take longer to close. However, they are meant to “address health and safety hazards, structural issues, and modernization” of homes that otherwise wouldn’t qualify.

While not ideal, if the required repairs are too extensive or the seller refuses to do them and other financing isn’t an option, sometimes the only choice is to cancel the deal.