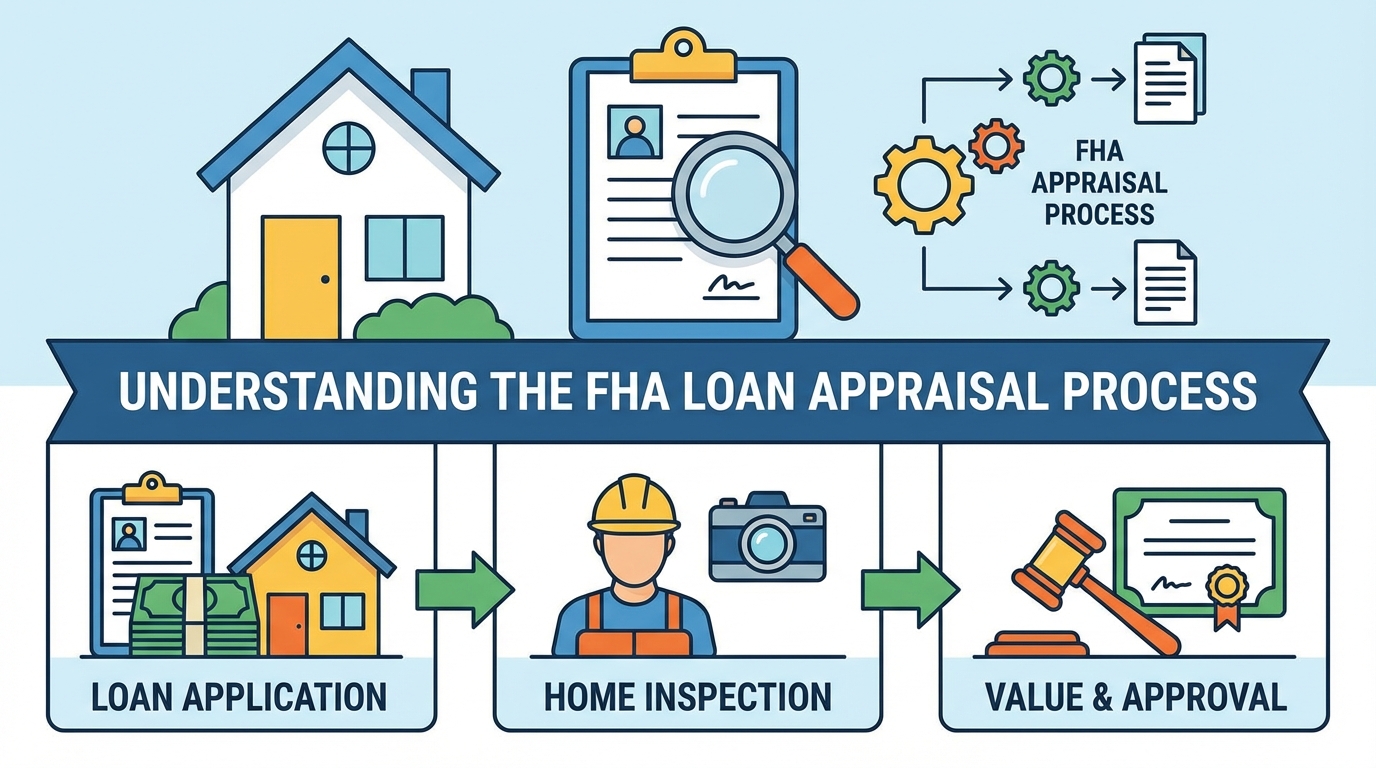

Appraisals are common in the real estate industry. Lenders generally require them to assess a home’s value before they’re willing to approve a loan on the property.

On FHA loans specifically, they’re used to not only determine a home’s fair market value, but also to ensure it meets all minimum property requirements set by the U.S. Department of Housing and Urban Development (HUD).

Appraisals are required on all FHA loans. Once a lender has sent an approved HUD appraiser to the property, they have 120 days in which to close the loan on the property. If that appraisal period expires, the lender will need to order a new appraisal before the loan can close.

One of the biggest goals of the appraisal is to ensure the property meets all FHA home requirements and safety standards, as well as any applicable state rules and regulations.

Specifically, FHA requires that the home:

There are also certain requirements that FHA appraisers must meet. First, they must be a state-certified appraiser and meet all minimum certification criteria set by the Appraiser Qualifications Board. They also comply with the Uniform Standards of Professional Appraisal Practice (USPAP) and cannot discriminate based on age, sex or race.

Check FHA Loan Requirements

Contact a home loan specialist here to determine if you're eligible. →

Aside from ensuring the property meets all FHA home requirements, an FHA appraiser will also look to determine the property’s value. To do this, they will evaluate the home’s condition, as well as analyze comparable properties in the area. These “comps” will include recently sold homes nearby with similar features, square footage and conditions.

The appraiser will then assign a value to the home, detail his or her findings in a report and send the report to the buyer’s mortgage lender for review. In many cases, appraisers will also take photos to show the lender the home’s condition.

The buyer is responsible for the cost of the home appraisal. These costs typically vary by market and depend on the size, age and condition of the home. Generally speaking, they fall between $300 and $500, in most cases.

FHA loans only require an appraisal -- not a home inspection. Still, HUD strongly encourages buyers to seek out a third-party inspection before purchasing their properties.

Though the appraisal will assess the home’s overall condition, it does not include a full evaluation of all the property’s appliances, systems and safety features. Home inspections are designed to be more in-depth, and they can also shed light on potential problems or repairs that may need to be made before move-in. Often, buyers can use home inspections to negotiate repairs or closing cost credits with the property’s seller.

FHA loans do not require pest inspections in most cases. In the event the FHA appraiser sees signs of termite damage or if the area is located in a known termite-heavy region, the lender might be required to send a termite inspector to the property.

As a buyer, you can also request a full pest or wood-destroying insect inspection from a local pest control company. These ensure the home you’re buying is free of any potential infestations that could pose health hazards (or cost significant amounts of money to treat).